Author: Guerric

Summer 2011. While attending a summer course on space studies, my fellow students and I watch the landing of the 135th and final mission of the American Space Shuttle program — Atlantis. At the time, SpaceX was an ambitious yet young company, which still had a lot to prove. That very morning, we had a lecture from Will Marschall, the CEO of the recently founded start-up Cosmogia. They had nothing but a bold vision of revolutionizing Earth observation with a flock of small modular satellites.

A little over a decade later, SpaceX has developed and operates the only vehicule of the western world capable to launch astronauts on orbit and bring them safely back home. Cosmogia, now rebranded Planet, has over 150 satellites in orbit collecting over 350 million square kilometers of imagery daily, and a market capitalization close to $1 billion. They have inspired dozens of startups in their wake. Market reports — for what they are worth — estimate that the global space economy reached a market size of around $424 billion in 2020, which is a 70% expansion since 2010. This boost is mostly attributable to a movement of commercialisation, which insiders call “NewSpace”.

Why the detour through summer 2011 to talk about nuclear? Mark my words: the conditions that allowed this breaking wave of innovations to take place in the space sector in the 2010s are currently met in the nuclear sector.

This is, at least, the thesis I will defind in this short article. In the first half, I examine the joint history of nuclear and space technologies. In the second half, I look at how the NewSpace movement shook the space sector, making new business cases possible and fueling an era of growth. Lastly, I go deeper into the weak signals that allow me to think that we are on the verge of a similar massive commercialization effort in the nuclear sector.

Brace yourself, exciting times ahead!

1. The atoms and space as Promethean technologies

1.1. Dark beginnings

A key common characteristic of nuclear and space technologies is an unprecedented potential for scalability. On the one hand, the energy released from nuclear fission is about a million times greater than that released by chemical reactions. On the other hand, satellites orbiting the Earth have unrestricted access to its entire surface.

It is thus no surprise that their practical uses were first explored in the context of war.

Space technologies soared from theoretical concepts to real-world applications with the development and use of the first long-range guided ballistic missile, the V2. It was the first artificial object to cross the Karman line, in June 1944, marking the beginning of the space age. Its design laid the foundation for future space launchers and intercontinental ballistic missiles (ICBM). Today still, the dual nature of space activities is indisputable. Earth observation (EO) satellites, for example, have become strategic assets for intelligence, surveillance, target acquisition, and reconnaissance (ISTAR) purposes.

The development of the atomic bomb was the other major technical endeavor of World War II. Robert Oppenheimer is famously quoted reciting Hindu scripture after witnessing the first detonation of a nuclear weapon, in July 1945, “now I am become Death, the destroyer of worlds”. The bombings of Hiroshima and Nagasaki would take place only one month later. Nuclear weapons are the most dangerous weapons of mass destruction ever conceived. Beyond weaponization, atomic energy remains today a critical tool for the defense sector, with applications such as nuclear propulsion.

1.2. Redemption, at the service of the common good

Despite these infamous beginnings, both technologies successfully transitioned from defense to civilian applications in the decade that followed.

In October 1957, Sputnik 1 became the first artificial satellite. Hannah Arendt would describe this event as “second in importance to no other, not even the splitting of the atom”. A couple of months later, in December, the first nuclear power plant exclusively dedicated to electricity production was connected to the grid.

Later on, two ambitious joint research facilities would be created in the hope of fostering broad international cooperation on these sensitive technologies.

On the one hand we have the International Space Station (ISS), a €100 billion microgravity laboratory orbiting the Earth. The ambition to build a modular space station was in talks since the early 1980s. The most important milestone towards its effective implementation is arguably the joint announcement made in September 1998 by American Vice-President Al Gore and Russian Prime Minister Viktor Chernomyrdin.

On the other hand is the International Thermonuclear Experimental Reactor (ITER), in France. It had also been in talks for a long time, since the late 1970s, until its development kicked off in October 1986 at the Reykjavik Summit. The total budget for its construction and operation is estimated to be around €25 billion, with some evaluations in excess of €60 billion.

To this day, the ISS and ITER are the most expensive research laboratories ever conceived. While they are often in the spotlight from a strictly technical perspective, both are actually powerful tools of the “serving science, serving peace” ideal. It is in that spirit that the crews of the ISS won the 2014 Peace of Westphalia award and that it is regularly nominated for the Nobel Peace Prize.

The peaceful use of nuclear and space technologies would actually become a major force for the greater good.

Despite the debates surrounding nuclear energy, the numbers speak for themselves: it is among the cleanest and most abundant energy sources we have access to. This explains its recent renaissance, including in Europe where the Commission recently recognized it as an essential building block toward our 2050 climate neutrality goal. In addition to energy, the atom also opened up a whole area of modern medicine, with cutting-edge diagnosis and treatment processes.

Space brought us critical infrastructures for global communications as well as positioning, navigation, and timing services. Satellites are also essential monitoring tools at every scale, from global weather and disaster management down to digital agriculture at the parcel level and greenhouse gas leak detection on infrastructures. These tools are all instrumental in our fight against climate change.

2. Towards a technological renaissance

2.1. A long road leading to a restricted club

Such benefits come with a high barrier to entry. Choices and investments required to access them must be done at the societal level.

Firstly, mastering and delivering on these technologies requires techno-scientific knowledge and an industrial base — specialized researcher centers, trained workforce, large-scale facilities, complex logistics, etc. Interestingly, there are some intersections between both fields: radiation environment, plasma physics, manufacturing methodologies, etc. all the way to practical applications such as radioisotope thermoelectric generators (RTG) for deep space exploration probes.

Secondly, the execution of both nuclear and space projects is typically long and financially intensive, which requires long-term vision and stability. This is exacerbated by a strong culture of safety and quality, embodied in countless standards, regulations, and overseeing agencies. Failure is not an option, be it because investments of that magnitude can only be done once (especially for space) or to ensure public health, safety, and security (especially for nuclear).

These hurdles drastically reduce the club of nations having access to these technologies, and the members of these clubs tend to work in silos. Contracts for nuclear and space projects are ordered by public authorities and executed by large domestic industrial players. There are only three large European primes for satellite manufacturing (i.e. Airbus Defence & Space, Thalès Alenia Space, and OHB). Similarly, there is only a handful of European nuclear engineering companies (e.g. Bouygues Construction, Ansaldo Energia, Siemens Energy, Framatome).

This privileged access is a power, which can be used as a diplomatic tool. Delivering a space system or a nuclear power plant to a foreign country is a sign of mutual trust. One party agrees to share some of its know-how and give access to powerful technology, while the other accepts a form of dependence on maintenance and repairs, training of specialized personnel, operational knowledge, etc. The Chinese support for Brazil’s Earth Resources Satellite program bears some resemblance to the recent contract signed by state-owned China National Nuclear Corp to build a nuclear power plant in Argentina.

2.2. NewSpace, the great shake-up of the space sector

The vertical description of the public authorities contracting large-scale projects to their domestic industry does not really hold anymore in the space sector. Over the past decade, the status quo has been challenged by the emergence of a parallel “NewSpace” sector which lowered the barriers to entry to space systems and enabled the emergence of new business use cases.

While this new economy is not entirely mature yet, the signs of its growing footprint are clearly visible. According to Space Capital, over $250 billion of private capital were invested in almost 1,700 space companies since 2012. Since venture funds typically have a 10-year horizon, the first fruits of these investments are being picked. Mergers, acquisitions, or exits are constantly in the news.

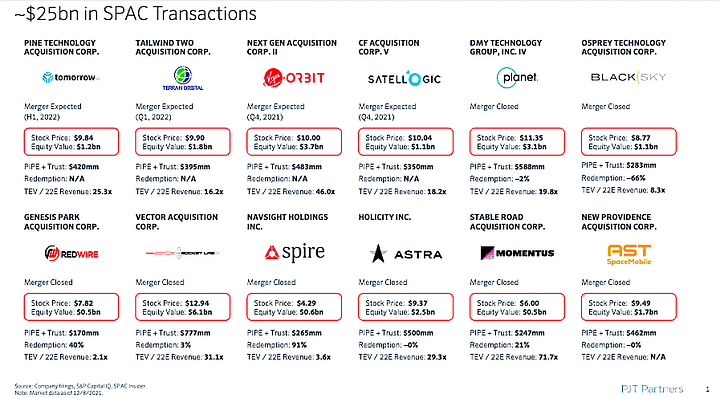

In 2021 only, twelve SPAC-enabled stock-market introductions were announced or concluded for a grand total valuation of $25 billion. Other investors seized the opportunity to consolidate “mini-primes”, such as the Redwire holding which already acquired eight companies since its creation in June 2020.

There are essentially three drivers that fuelled the NewSpace economy.

First, a new approach to space systems focused on miniaturization and modularity. Small satellites have always been around — Sputnik 1 weighed only about 80 kg. However, it is only in the 1980s that pioneering companies such as Surrey Satellite Technology Ltd (SSTL) started to use them to deliver cheaper and faster space systems.

The real accelerator came with the invention of the CubeSat standard, a cubic module of 10 cm on side, which can be assembled to form larger satellites. It started modestly, in 1999, as an assignment for graduate students in California. Over 1,800 of these tiny satellites have been launched up to now according to the Nanosats Database. Since 2013, more than half of launches are for non-academic purposes. This growth fuelled an entire market for small satellites, up to hundreds of kg, that enabled the emergence of a brand-new supply chain.

Second, the active involvement of extremely wealthy entrepreneurs eager to take risks and challenge the status quo. The examples are legion. In the 1990s, already, Bill Gates tried to disrupt the telecommunication industry with Teledesic, a mega-constellation of small satellites. A few years later, Jeff Bezos founded Blue Origin (2000) and Elon Musk founded SpaceX (2002).

A couple of years later still, Anousheh and Amir Ansari made a multimillion-dollar donation to the X Prize. This would fuel a race for space, that would eventually be won by a team funded by Paul Allen. Their spacecraft concept would be commercialized for tourism through Virgin Galactic (2004) by Richard Branson, who would expand his space portfolio through the creation of Virgin Orbit (2017). Paul Allen would also pursue his interest with Stratolaunch Systems (2011). The list goes on. Through their ventures, they catalyzed a new generation of young entrepreneurs.

Last but not least, several technological innovations. These mostly concern software: big data, artificial intelligence, digitalization, cloud computing, lean methodologies, etc. — all of which support scalable business cases. The space sector is now so reliant on software infrastructures that a cloud service provider like Amazon Web Services is operating its own network of ground stations to service the satellite industry.

2.3. NewNuc, the next tsunami of innovation?

Given the striking similarities between atomic and space technologies, I would argue that the same disruption is likely to take place in the nuclear sector. The same signs as those for the emergence of NewSpace are already visible, albeit with some temporal delay. Could it be the onset of a NewNuc economy? Or NewNuclear? NewClear? NewK? Time will tell which is the catchiest. One thing is for sure; it’s coming.

Let’s start simple. Miniaturization and modularity, does that ring a bell? Replacing large projects, heavy in resource consumption, with multiple smaller but easier-to-handle units? What about Small Modular Reactors (SMR)? Of course, they’re a different scale of investment than small satellite missions. Nonetheless, in relative terms, it is a relevant comparison: a size reduction in the order of 10–20x (e.g. cost, mass, power).

The involvement of wealthy entrepreneurs is also starting to pick up. The same names are popping up: Bill Gates founding TerraPower in 2006, Jeff Bezos investing in General Fusion since 2011, etc. In addition to them, however, a new generation of tech moguls is getting involved. One particularly striking example is Sam Altman, CEO of OpenAI and former president of Y Combinator, who invested $375 million into Helion last November. Other wealthy individuals took part in the funding round, including Facebook co-founder Dustin Moskovitz and Peter Thiel’s Mithril Capital. Another example is the French Perrodo family investing in Rolls Royce’s SMR technology plans

Last but not least, technological innovations seem to be increasingly making their way into the nuclear industry. Tools such as virtual reality, augmented reality, artificial intelligence, and machine learning are making their way to technical conferences. Digital transformation was actually identified by the Nuclear Energy Agency (NEA) among the top three technology approaches that could be implemented to deliver rapid cost reductions in the short term for the development of third-generation reactor projects. Start-ups like Siteflow are leading the charge to accelerate the transition.

Could it be the start of a new chapter? Will we see the same breaking wave of innovation shaking the nuclear energy sector, as it did for the space sector over the last decade?

My bet is that the answer is yes.